|

There has certainly been a lot of talk over the past few days about just who gets what after the passage and the signing of coronavirus economic relief plan last week. Many are now expecting a check from the government, while many others are wondering if they will get one. That’s been one of the bigger headlines, because hey, free money at a time when many people could really use it.

Even then, though, it can be a little confusing about just how much one will receive. It has also become so big that a lot of other benefits have received less notice. These include things like unemployment benefits, some student loan help, changes in how you can get money out of a retirement account, and a potential added tax deduction for charitable donations. There is so much information that it can feel overwhelming, but pushing through it is worth it because when used correctly it can mean that many affected during these economic struggles can end up in similar (or even better) positions than they were before the crisis. This will take a little patience and a few difficult weeks, but that just means it is even more important to utilize the help that is being offered. Just how this works can be different depending on your personal situation. The New York Times has a great Q&A about the stimulus package located here that answers many questions of different types. Here is to hoping that you and those close to you are staying safe and well.

0 Comments

Updated 4/26/2020

The funding for this program has been replenished as of 4/24. If you have not submitted an application, we recommend you work with a local community bank for better service, as the national banks seem to be overwhelmed. ------------------------------- During a time when many are not working and increasing numbers of businesses are thinking they may have to lay off employees, a government program for loans to maintain payroll during the current economic crisis is a novel and welcome move. The fact that some of the money borrowed could then be forgiven (depending on what you use the money on, especially if payroll) makes the program even more attractive. The program is called the Paycheck Protection Program and was part of the $2.2 trillion coronavirus stimulus bill signed into law last week. In fact, $349 billion of that total was set aside for the PPP. If you want to know more about how this works, this article from Fortune gives a very good summary of the details. Getting one of these loans will involve applying through an institution that already offers SBA loans (starting April 3). The best bet is to contact your current bank and inquire about the program. Some other issues of note, if you are also planning on using the employee retention tax credit, you cannot do both that and get PPP loan forgiveness. And if you already applied for an EIDL loan, it is not an either-or proposition, you can also apply for a PPP loan and the EIDL is expected to be rolled into if that turns out to make sense for you. For official information from the Senate on this, click here. In a situation where any extra time to take care of responsibilities (and pay bills) feels like a giant gift, the IRS has officially suspended the tax filing deadline until July 15 and also suspended tax payments due originally due on April 15 until that date.

These two actions are separate, because even when you file your taxes on time, if you owe the IRS money but do not pay it by the deadline, you immediately start accruing fees and interest. With the actions paired like this, it really is a complete three-month relaxation. Also during this time, the IRS has set up a webpage where it will gather relevant data related to the coronavirus emergency. During a time when the news cycle seems faster than ever and rumors and first steps can be reported as final actions, having a place like this where you can go and get the real information directly from the source can be necessary to see through/interpret rhetoric read elsewhere. This webpage is located at irs.gov/coronavirus. Please note that many states, including Pennsylvania, have also extended the due dates for tax returns, but you should check with your tax preparer to see if your state is included. Governor Wolf and Rep. Dan Moul announce emergency loans are now available to small businesses with less than 100 employees. Information on the COVID-19 Working Capital Access Program (CWCA) can be found via the link below. This loan does not have an easy to access application, but must be requested through your local county CEDO. Please review the Fact Sheet for more information on applying for this loan. The COVID-19 Working Capital Access (CWCA) Program is administered by the Pennsylvania Industrial Development Authority (PIDA) and provides critical working capital financing to small businesses located within the Commonwealth that are adversely impacted by the COVID-19 outbreak. All CWCA loan applications must be submitted through a Certified Economic Development Organization (CEDO). For the list of CEDO’s operating within Pennsylvania, please refer to the CEDO webpage. Uses - Working capital, which for purposes of this program is considered capital used by a small business for operations, excluding fixed assets and production machinery and equipment. Eligibility - An eligible small business enterprise is a for-profit corporation, limited liability company, partnership, proprietorship or other legal business entity located in the Commonwealth of Pennsylvania and having 100 or fewer full-time employees worldwide at the time of submission of the application. For purposes of this program a retail/service enterprise is defined as a for-profit business entity that is involved in the business-to-business service, business-to-public service, mercantile, commercial, or point of sale retail sectors. An agricultural producer is defined as a business involved in the management and use of a normal agricultural operation for the production of a farm commodity. A “farm commodity” is any Pennsylvania-grown agricultural, horticultural, aquacultural, vegetable, fruit, and floricultural product of the soil, livestock and meats, wools, hides, furs, poultry, eggs, dairy products, nuts, mushrooms, honey products, and forest products. Funding and Terms - The maximum loan amount is $100,000. Loan terms are three years with a 12-year amortization. In addition, 1) No payments will be due and payable during the first year, 2) Principal and if applicable, interest payments will be due monthly for years two and three, and 3) A balloon payment will be due and payable at the end of the third year. The interest rate for the program is 0% except for agricultural producers in which case the interest rate is 2% fixed for the life of the loan. How to Apply - Loan applications are packaged by a CEDO that services the county your business is located in. The CEDO will work with you to determine if the CWCA loan program can assist with financing the needs of your business and will discuss with you in detail how the application process works. Visit the Certified Economic Development Organization webpage for a complete listing by county.

Questions about the program can also be directed to 717.783.5046. The Philadelphia COVID-19 Small Business Relief Fund offers grants or zero-interest loans to Philadelphia small businesses impacted by the COVID-19 pandemic. The program, administered by the Department of Commerce and Philadelphia Industrial Development Corporation (PIDC), aims to:

Please refer to the application details for more information about what you'll need to complete your application. Click here to apply: https://phila-uyims.formstack.com/forms/philadelphia_covid_19_small_business_relief_fund More information about this program - https://www.phila.gov/programs/philadelphia-covid-19-small-business-relief-fund/?mc_cid=e610c84755&mc_eid=0e0c66297c

The state of Florida has activated the Florida Small Business Emergency Bridge Loan program.

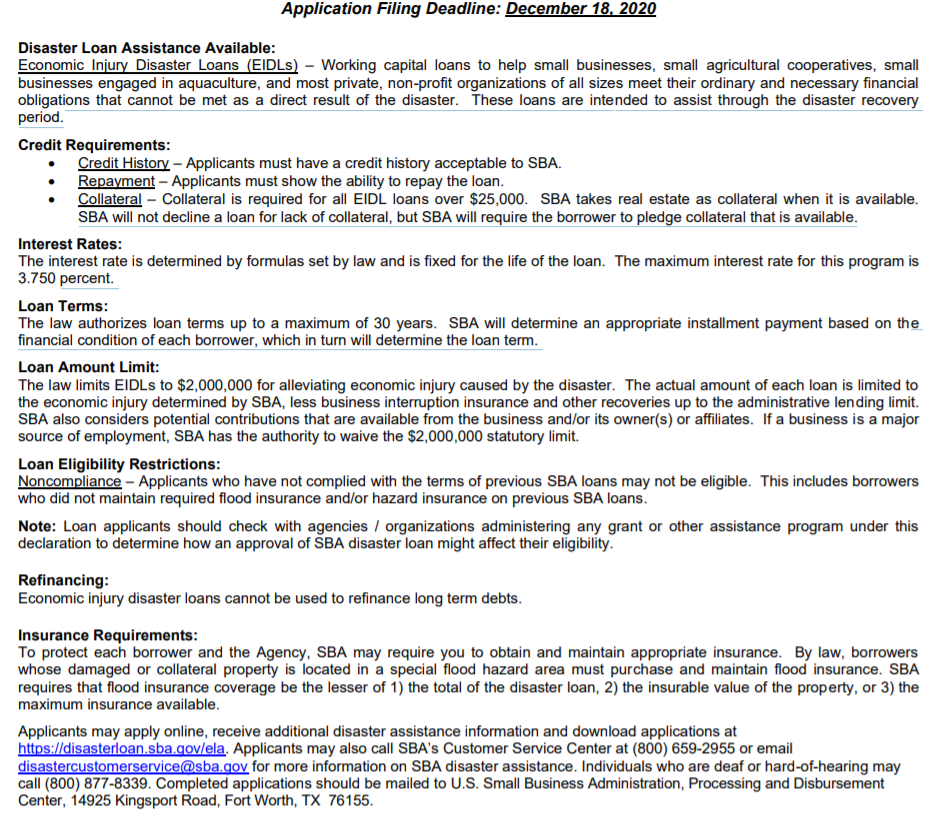

Details can be found: https://floridadisasterloan.org/ The Florida Small Business Emergency Bridge Loan Program is currently available to small business owners located in all Florida counties statewide that experienced economic damage as a result of COVID-19. These short-term, interest-free working capital loans are intended to “bridge the gap” between the time a major catastrophe hits and when a business has secured longer term recovery resources, such as sufficient profits from a revived business, receipt of payments on insurance claims or federal disaster assistance. The Florida Small Business Emergency Bridge Loan Program is not designed to be the primary source of assistance to affected small businesses, which is why eligibility is linked pursuant to other financial sources. Note: Loans made under this program are short-term debt loans made by the state of Florida using public funds – they are not grants. Florida Small Business Emergency Bridge Loans require repayment by the approved applicant from longer term financial resources. Application can be found: https://floridadisasterloan.org/application/ As of 3/21/2020, the SBA has opened the SBA Disaster Loan due to COVID-19 to many states, including PA, DE, NY, NJ, CT, MA, DC, MD, VA, NC, SC, GA, and FL. You can search for your area here - https://disasterloan.sba.gov/ela/Declarations/Index This loan is available to businesses as “Working capital loans to help small businesses, small agricultural cooperatives, small businesses engaged in aquaculture, and most private, non-profit organizations of all sizes meet their ordinary and necessary financial obligations that cannot be met as a direct result of the disaster. These loans are intended to assist through the disaster recovery period.” This loan has a 3.75% interest rate (2.75% for nonprofits) with a repayment term of up to 30 years. Note that this is not a comprehensive list or instructions, but should help you prepare for your application. Businesses will be required to provide personal and business financial information including, but not limited to:

READY TO APPLY? disasterloan.sba.gov From the U.S. SMALL BUSINESS ADMINISTRATION FACT SHEET – ECONOMIC INJURY DISASTER LOANS  |

ArchivesCategories |

RSS Feed

RSS Feed